Are you considering a 401k loan from Merrill? If so, you're not alone. Many individuals turn to their retirement savings as a source of funds in times of financial need. However, before making any decisions, it's crucial to understand the ins and outs of Merrill 401k loans. In this comprehensive guide, we'll walk you through all the essential details, eligibility criteria, pros and cons, and much more.

What is a Merrill 401k Loan?

A Merrill 401k loan is a loan that allows you to borrow money from your 401k retirement account. Unlike a regular loan, where you would borrow money from a financial institution, a 401k loan allows you to borrow from your retirement savings. The maximum amount you can borrow from your Merrill 401k account is typically 50% of your vested balance or $50,000, whichever is less.

One of the key advantages of a Merrill 401k loan is that there are no credit checks required. This means that even if you have a low credit score or a less-than-perfect credit history, you may still be eligible to borrow from your 401k. Additionally, the interest rates on 401k loans are typically lower compared to other types of loans, making them an attractive option for individuals in need of immediate funds.

Subheading 1: Reasons for Taking a Merrill 401k Loan

There are several reasons why individuals may choose to take a 401k loan from Merrill. One common reason is to cover unexpected expenses, such as medical bills or home repairs. By borrowing from their retirement savings, individuals can access the funds they need without resorting to high-interest credit cards or other forms of debt.

Another reason individuals may opt for a Merrill 401k loan is to consolidate high-interest debt. If you have multiple outstanding loans or credit card balances with high interest rates, taking a 401k loan can help you pay off those debts and potentially save money on interest payments. However, it's important to consider the potential risks and consequences before using your retirement savings to pay off debt.

Some individuals may also choose to take a 401k loan to make a down payment on a home. This can be particularly beneficial for first-time homebuyers who may not have enough savings for a traditional down payment. By borrowing from their 401k, they can secure a more favorable mortgage rate and potentially save money in the long run.

Subheading 2: Repayment Terms

When you take a Merrill 401k loan, you will typically have up to five years to repay the loan. However, if the loan is used to purchase a primary residence, the repayment period may be extended to up to 15 years. It's important to note that the repayment terms may vary depending on your specific plan, so it's crucial to carefully review the terms and conditions of your 401k loan.

401k loans are typically repaid through regular payroll deductions. This means that a portion of your paycheck will be deducted to repay the loan. It's important to consider the impact of these deductions on your monthly budget and cash flow. However, one advantage of 401k loan repayments is that the interest you pay goes back into your own retirement account, rather than to a financial institution.

Additionally, it's crucial to understand the potential consequences of defaulting on your 401k loan. If you fail to make the required loan payments, the outstanding balance may be considered a distribution from your retirement account. This could result in taxes and penalties, significantly impacting your overall retirement savings. Therefore, it's essential to make timely and consistent payments to avoid any potential pitfalls.

Eligibility and Application Process

To be eligible for a Merrill 401k loan, you must meet certain criteria set by your employer and the plan administrator. Generally, you must be an active employee of the company sponsoring the 401k plan. Furthermore, you must have a vested balance in your 401k account, meaning that you have earned the right to the employer contributions made to your account.

Subheading 1: Employment Status

Typically, you must be a current employee of the company to be eligible for a 401k loan. If you leave your job or are terminated, you may be required to repay the outstanding balance of your loan within a specific timeframe. Failing to do so may result in the loan being considered a distribution and subject to taxes and penalties.

Subheading 2: Vested Balance

Your vested balance refers to the portion of your 401k account that you are entitled to keep, even if you leave your job. Some employers have a vesting schedule, which means that your employer's contributions to your 401k account may vest over a certain period of time. To be eligible for a 401k loan, you must have a vested balance in your account.

Subheading 3: Loan Restrictions

While 401k loans offer flexibility and convenience, there are some restrictions that you need to be aware of. For instance, you can only borrow up to 50% of your vested balance or $50,000, whichever is less. This limit applies to all 401k loans you have, regardless of the number of plans you participate in.

Furthermore, there may be limitations on the number of loans you can have outstanding at any given time. Some plans may only allow one loan at a time, while others may permit multiple loans. It's essential to review your plan's rules and consult with the plan administrator or a financial advisor to understand the specific restrictions that apply to your situation.

Subheading 4: Loan Application Process

The loan application process for a Merrill 401k loan typically involves several steps. First, you will need to contact the plan administrator or log into your account online to access the necessary loan application forms. These forms will require you to provide personal information, including your name, address, Social Security number, and the amount you wish to borrow.

Once you have completed the application forms, you will need to submit them to the plan administrator for review. The administrator will assess your eligibility and ensure that all required documentation is provided. This may include proof of employment, the most recent account statement, and any other supporting documents as required by your plan.

After the loan application is reviewed and approved, the funds will be disbursed to you typically within a few business days. It's important to note that the loan amount will be subtracted from your 401k account balance, which may impact your investment allocations and potential earnings.

Pros and Cons of Merrill 401k Loans

Before deciding to take a 401k loan, it's important to weigh the advantages and disadvantages. While a 401k loan may provide immediate access to funds, it's crucial to consider the impact on your retirement savings and the potential risks involved.

Subheading 1: Pros of Merrill 401k Loans

One major advantage of a Merrill 401k loan is that there are no credit checks involved. This means that individuals with less-than-perfect credit can still qualify for a loan. Additionally, the interest rates on 401k loans are typically lower compared to other forms of debt, making them a more affordable option for borrowing.

Another advantage is that the interest you pay on a 401k loan goes back into your own retirement account. This can help offset the potential loss of investment earnings while the loan is outstanding. Furthermore, the loan repayments are typically deducted from your paycheck, making it easier to manage and ensuring consistent payments.

Subheading 2: Cons of Merrill 401k Loans

One significant disadvantage of a 401k loan is the potential impact on your retirement savings. When you borrow from your 401k, you are essentially taking money out of your future nest egg. This means that the funds you borrow will no longer be invested and potentially earning returns, which can hinder the growth of your retirement savings.

Another drawback is the risk of defaulting on the loan. If you are unable to make the required loan payments, the outstanding balance may be considered a distribution. This can result in taxes and penalties, significantly reducing the amount you receive when you retire. Defaulting on a 401k loan should be avoided at all costs to protect your long-term financial well-being.

Furthermore, taking a 401k loan may limit your ability to contribute to your retirement account during the repayment period. This can disrupt your retirement savings strategy and potentially impact employer matching contributions, leading to a loss of free money. It's essential to carefully consider the potential consequences and the impact on your overall retirement goals before taking a 401k loan.

Repayment Options and Strategies

When it comes to repaying your Merrill 401k loan, it's important to understand the available options and develop a strategy that aligns with your financial situation and goals. By managing your loan repayment effectively, you can minimize the impact on your retirement savings and ensure timely payments.

Subheading 1: Repayment Terms and Interest Rates

401k loans typically have a maximum repayment period of five years. However, if the loan is used to purchase a primaryresidence, some plans may allow for an extended repayment period of up to 15 years. It's crucial to review the specific terms and conditions of your Merrill 401k loan to understand the repayment timeline.

During the repayment period, you will be required to make regular payments, usually on a monthly basis. These payments will include both principal and interest. The interest rates on 401k loans are generally lower compared to other types of loans, making them a more affordable borrowing option. However, it's important to note that the interest you pay on a 401k loan is not tax-deductible.

To determine the exact amount of your loan payments, you can use an online loan calculator or consult with the plan administrator. By knowing the repayment amount, you can budget accordingly and ensure that you have sufficient funds to make the payments on time.

Subheading 2: Loan Repayment Strategies

Managing your Merrill 401k loan repayment effectively is crucial to avoid default and minimize the impact on your retirement savings. Here are a few strategies to consider:

1. Create a Repayment Plan

Start by creating a detailed repayment plan that outlines the amount and frequency of your loan payments. By mapping out your repayment schedule, you can ensure that you stay on track and never miss a payment. Consider setting up automatic payments to simplify the process and avoid any potential late fees.

2. Cut Expenses

During the repayment period, it may be beneficial to cut back on discretionary expenses and redirect those funds towards your loan payments. Look for areas where you can reduce spending, such as eating out less frequently or cutting back on entertainment expenses. By making small sacrifices, you can allocate more money towards repaying your 401k loan.

3. Increase Income

If possible, consider finding ways to increase your income to accelerate the loan repayment process. This could involve taking on a part-time job or freelance work, selling unused items, or finding other sources of additional income. By generating extra funds, you can make larger loan payments and potentially repay the loan ahead of schedule.

4. Prioritize Loan Repayment

Make repaying your Merrill 401k loan a top priority. While it may be tempting to focus on other financial goals or expenses, it's essential to remember that your retirement savings are at stake. By prioritizing your loan repayment, you can ensure that you protect your long-term financial well-being and minimize any potential penalties or taxes.

5. Avoid Borrowing Again

Once you have repaid your Merrill 401k loan, strive to avoid borrowing from your retirement savings again in the future. Instead, focus on building an emergency fund and exploring other financial options to address any unexpected expenses. By reducing reliance on 401k loans, you can preserve your retirement savings and maintain financial stability.

Alternatives to Merrill 401k Loans

While a Merrill 401k loan can be a viable option for accessing funds, it's important to explore alternative solutions before making a decision. Depending on your financial situation and needs, there may be other options available that are more suitable for your circumstances.

Subheading 1: Personal Loans

If you have a good credit score, a personal loan from a bank or credit union may be a viable alternative to a 401k loan. Personal loans typically have fixed interest rates and repayment terms, allowing you to borrow a lump sum and make regular payments over a specified period. It's important to compare interest rates and repayment terms to determine the most cost-effective option for your needs.

Subheading 2: Home Equity Loans or Lines of Credit

If you own a home and have built up equity, you may consider a home equity loan or line of credit. These loans allow you to borrow against the value of your home and can provide access to larger sums of money. However, it's important to note that your home serves as collateral for these loans, putting it at risk if you fail to make the required payments.

Subheading 3: Cash-Out Refinancing

If you have a mortgage, cash-out refinancing may be an option worth exploring. This involves refinancing your existing mortgage for a higher amount than what you currently owe and receiving the difference in cash. Cash-out refinancing often comes with lower interest rates compared to other forms of borrowing, but it's essential to carefully evaluate the terms and potential fees involved.

Subheading 4: Emergency Savings

Building an emergency savings fund is one of the most effective ways to avoid the need for a 401k loan or other forms of borrowing. By setting aside a portion of your income regularly, you can create a safety net to address unexpected expenses. Aim to save at least three to six months' worth of living expenses in an easily accessible and low-risk account.

Subheading 5: Financial Assistance Programs

In some cases, you may be eligible for financial assistance programs that can provide temporary relief during challenging times. These programs may include unemployment benefits, rental assistance, or low-income support. Research and explore the available options in your area to determine if you qualify for any assistance programs that can help address your financial needs.

Impact on Retirement Savings

One of the most critical considerations when contemplating a Merrill 401k loan is the impact it can have on your retirement savings. While it may provide immediate financial relief, it's essential to evaluate the long-term consequences and ensure that borrowing from your 401k aligns with your retirement goals.

Subheading 1: Loss of Potential Growth and Compounding

When you take a 401k loan, the borrowed funds are no longer invested in your retirement account. This means that you miss out on potential growth and compounding that could significantly increase your retirement savings over time. It's important to remember that your retirement account is designed to provide for your future, and any early withdrawals or loans may hinder your ability to achieve your desired retirement lifestyle.

Subheading 2: Disruption of Regular Contributions

Contributing regularly to your 401k is crucial for building a substantial retirement fund. By taking a loan, you may need to reduce or suspend your regular contributions to accommodate the loan repayment. This disruption can result in missed employer matching contributions and slower overall growth of your retirement savings. It's essential to assess the impact on your retirement strategy and consider alternative ways to address your immediate financial needs.

Subheading 3: Taxes and Penalties

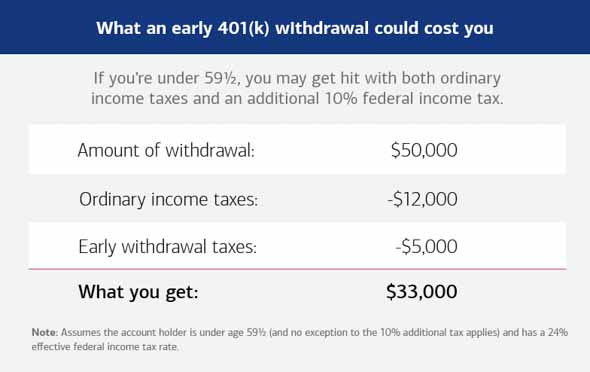

If you fail to repay your 401k loan as required or default on the loan, the outstanding balance may be considered a distribution from your retirement account. This distribution is subject to income taxes and potentially early withdrawal penalties if you're under the age of 59 ½. These taxes and penalties can significantly reduce the amount you receive when you retire, potentially impacting your financial security in later years.

Subheading 4: Long-Term Financial Planning

Before taking a Merrill 401k loan, it's crucial to evaluate your long-term financial planning and consider alternative options. Speak with a financial advisor to assess your overall financial situation and explore other strategies for meeting your immediate financial needs without compromising your retirement savings. It's important to have a comprehensive plan in place that aligns with your goals and ensures a secure financial future.

Tax Implications of Merrill 401k Loans

When it comes to 401k loans, it's important to understand the potential tax implications to avoid any surprises when tax season arrives. While 401k loans are not subject to income taxes when you borrow the funds, certain circumstances can result in taxes and penalties.

Subheading 1: Loan Repayment and Taxes

When you repay a Merrill 401k loan, you are using after-tax dollars. This means that the loan repayments do not provide any additional tax benefits. It's important to account for the loan repayments in your budget and consider them as part of your regular expenses.

Subheading 2: Consequences of Defaulting

If you default on your 401k loan and the outstanding balance is considered a distribution, it becomes subject to income taxes. The distribution may be treated as taxable income for the year in which it occurs. Additionally, if you're under the age of 59 ½, you may also face an early withdrawal penalty of 10% on the distributed amount.

Subheading 3: Tax Reporting

When you take a 401k loan, it's important to keep track of your loan repayments and any outstanding balances. During tax season, you will need to report the loan on your tax return using Form 1099-R. The form will show the amount of the loan and any interest paid during the year. Consult with a tax professional or review the IRS guidelines to ensure accurate reporting of your 401k loan.

Subheading 4: Tax Considerations for Early Withdrawals

In some cases, individuals may consider withdrawing funds from their 401k instead of taking a loan. It's important to note that early withdrawals from a 401k account are generally subject to income taxes and a potential early withdrawal penalty if you're under the age of 59 ½. If you find yourself in a situation where you need to withdraw funds from your 401k, it's crucial to consult with a tax professional to understand the tax implications and explore any potential exceptions or alternatives that may be available to you.

Frequently Asked Questions

When it comes to Merrill 401k loans, individuals often have questions and concerns. Here are some frequently asked questions that can provide further clarity on this topic:

1. Can I borrow from my Merrill 401k if I have a low credit score?

Yes, one of the advantages of a 401k loan is that there are no credit checks involved. Your credit score does not impact your eligibility for a Merrill 401k loan. However, it's important to note that borrowing from your 401k should be done cautiously and as a last resort to avoid potential negative consequences on your retirement savings.

2. Can I have multiple 401k loans at the same time?

The rules regarding multiple 401k loans vary depending on your specific plan. Some plans may allow multiple loans, while others may restrict you to only one outstanding loan at a time. It's important to review your plan's guidelines or consult with the plan administrator to understand the specific restrictions that apply to your situation.

3. Can I repay my Merrill 401k loan early?

Yes, in most cases, you can repay your Merrill 401k loan earlier than the set repayment period. Early repayment can help you save on interest payments and reduce the impact on your retirement savings. However, it's important to review your specific loan terms and confirm with the plan administrator if there are any prepayment penalties or restrictions in place.

4. Can I continue making contributions to my 401k while repaying a loan?

While it's generally allowed to continue making contributions to your 401k while repaying a loan, it's important to review your plan's rules and guidelines. Some plans may restrict or suspend contributions until the loan is fully repaid. It's crucial to understand the impact of loan repayments on your overall retirement savings strategy and adjust contributions accordingly.

5. What happens to my Merrill 401k loan if I leave my job?

If you leave your job, whether voluntarily or involuntarily, the outstanding balance of your Merrill 401k loan may become due. Failing to repay the loan within a specified timeframe could result in the loan being considered a distribution. This distribution may be subject to taxes and penalties, significantly impacting your retirement savings. It's essential to carefully evaluate your options and consult with a financial advisor to understand the best course of action in this situation.

Risks and Considerations

While a Merrill 401k loan may provide immediate financial relief, it's crucial to consider the potential risks and consequences associated with borrowing from your retirement savings.

Subheading 1: Impact on Retirement Savings

One of the most significant risks of a 401k loan is the potential impact on your retirement savings. By borrowing from your 401k, you are essentially depleting your future nest egg and reducing the potential growth of your retirement funds. It's important to carefully evaluate the long-term consequences and consider alternative solutions to address your immediate financial needs.

Subheading 2: Potential Loss of Employer Contributions

When you take a 401k loan, you may be required to reduce or suspend your regular contributions to accommodate the loan repayment. This can result in missed employer matching contributions, which can significantly impact the growth of your retirement savings. It's essential to carefully weigh the potential loss of employer contributions against your immediate financial needs to make an informed decision.

Subheading 3: Default and Tax Consequences

If you default on your Merrill 401k loan, the outstanding balance may be considered a distribution and subject to taxes and penalties. This can significantly reduce the amount you receive when you retire, potentially affecting your financial security in later years. It's crucial to make timely and consistent loan payments to avoid defaulting on your loan and protect your retirement savings.

Subheading 4: Opportunity Cost

Borrowing from your 401k comes with an opportunity cost. The funds you borrow are no longer invested and potentially earning returns. This means that you miss out on the potential growth and compounding that could significantly increase your retirement savings over time. It's important to carefully evaluate the potential opportunity cost and consider alternative options before deciding on a 401k loan.

Subheading 5: Long-Term Financial Goals

Before taking a Merrill 401k loan, it's crucial to assess your long-term financial goals and evaluate the impact of borrowing from your retirement savings. Consider alternative solutions, such as building an emergency fund or exploring other forms of borrowing, that can address your immediate financial needs without compromising your long-term financial well-being. It's important to make decisions that align with your overall financial strategy and goals.

Final Thoughts

While a Merrill 401k loan can provide immediate access to funds, it's essential to carefully evaluate the potential risks and consequences before making a decision. Consider alternative options, assess the impact on your retirement savings, and consult with a financial advisor to ensure that you make an informed choice that aligns with your long-term financial goals.

Remember, borrowing from your 401k should be done cautiously and as a last resort. Your retirement savings are crucial for your financial security in later years, and any decision that impacts those savings should be thoroughly considered. By weighing the pros and cons, understanding the eligibility criteria, and exploring alternative solutions, you can make a well-informed decision that best suits your individual circumstances and financial well-being.

Comments

Post a Comment